Meta 4Q'23 Update

Disclosure: I own shares and 2025 January $50 Call Options of Meta

By 3Q’23 earnings, almost everyone understood Meta’s turnaround; the layoffs were behind us, topline growth was accelerating, and thanks to Meta’s “efficiency”, margins were expanding.

Yet, the stock has gone up another ~60% since 3Q’23 earnings (including AH earnings reaction today). Despite being one of the big tech companies, the stock’s volatility in both directions has been nothing short of dizzying for investors. From ~75% drawdown in 2022 to ~+400% from the bottom in just 15 months, there was never quite a dull moment for Meta’s shareholders!

Here are my highlights from tonight’s call.

Users

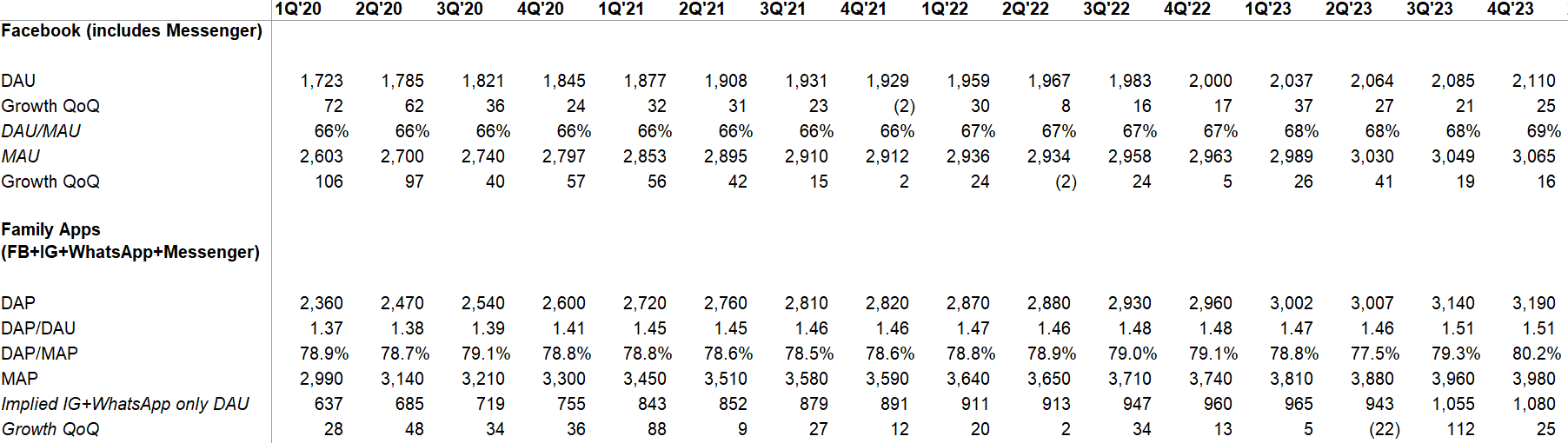

Take a look at the Facebook’s DAU or MAU number for the last time because Meta will stop reporting them from next quarter.

Investors usually assume the worst when any important KPI gets deprecated by the company. Thankfully, along with Family “Daily Active People” (DAP), Meta will report YoY changes in ad impressions and average price per ad by region.

I suspect a granular region level data may prove to be more helpful for investors to gauge Family of App’s (FOA) health than what the deprecated data was providing us.

Engagement

DAU/MAU engagement improved QoQ in every single region. Overall DAU/MAU ratio has been inching up for the last eight consecutive quarters.

ARPU

While ARPU exhibited considerable strength, please note the material weakness in YoY comparison and hence, 2-yr CAGR is likely better reflective of long-term trend. As you can see below, we have one more quarter of easy comp ahead of us after which growth may start to mirror closer to long-term trends.

Annual ARPU (calculated as ad revenue divided by FB MAU) in North America reached ~$220 in 2023 which is a staggering number. While that can also make investors nervous wondering how much larger it can possibly be, it does seem Meta’s ad infra continues to get better which is essential for further runway for ARPU:

Our approach to optimizing ad levels in our apps has become increasingly sophisticated over the years as we've developed a better understanding of the optimal place, time and person to show an ad, which has enabled us to adopt a more dynamic approach to serving ads. We expect to continue that work going forward, while services with relatively lower levels of monetization like video and messaging will serve as additional growth opportunities

Ad revenue

Number of ad impression grew by 21% YoY whereas average price per ad increased by 2% YoY, driven by “advertiser demand and currency tailwinds, which were partially offset by strong impression growth, particularly from lower-monetizing services and regions”

.

China-based advertisers was 10% overall revenue for Meta in 2023 and contributed 5 percentage point of growth. After last quarter, investors started worrying about sustainability of this growth. While the stock price trajectory since then makes me think such concern has largely dissipated, I suspect it can come back at a moment’s notice anytime we start to see softness from these China-based advertisers.

Segment Reporting

Overall 4Q’23 revenue was +25% YoY(+22% FXN) whereas total expenses was -8% YoY.

On a 2-yr CAGR basis, Meta’s topline increased by 9.1% in 4Q’23. For context, Google Search revenue grew by 5.3% and Google advertising increased by 3.4% during the same time!

FOA posted ~80% incremental operating margin in 4Q’23 vs 4Q’21 (just as it did for 3Q’23 vs 3Q’21). For the second consecutive quarters, FOA had >50% operating margin. This is damn impressive of course, but let me change gear a little.

Looking at such margins, it reminded me about Zuck’s appearance at Senate hearing yesterday. While the hearing is bit of a circus, I cannot help but think a business with >50% operating margin can, should, and must do more than what Meta does today to protect their users from harm’s way. While this may depress near-term margins, it may be of paramount importance for long-term health of the business; in fact, it may further entrench these big tech’s moats even if it leads to lower margins in the near term.

To be clear, unlike most people, I am far from convinced that usage of social media is harming today’s teens, but I do think Meta may need to do more as society’s (and regulators) expectation from big tech evolves as they get bigger and bigger. The increasing presence of scammy ads has also been disappointing and concerning to see.

Okay, back to financials now.

Other revenue, which includes “business messaging” from WhatsApp, stood out to me for its pace of growth. Although it’s a small base for now, it increased by 82% YoY (2-yr CAGR 47%) and will be interesting to see if the momentum persists in 2024.

Reality Labs remains largely a cause of concern for investors. While it exceeded $1 Bn revenue for the first time, thanks to Quest 3 and Quest 2 sales during Christmas season, losses have no sign of peaking. In fact, Meta mentioned again for 2024, “for Reality Labs, we expect operating losses to increase meaningfully year-over-year due to our ongoing product development efforts in AR/VR and our investments to further scale our ecosystem.”

I know some Meta bulls are tempted to look at FOA and try to imagine some SOTP by assigning Reality Labs valuation of zero. I strongly discourage you to do that as I think it should be clear by now that despite what you may have read about Meta “pivoting from Metaverse to AI”, that is pure fiction. Meta remains fully committed to AR/VR and with Apple’s entry to this space, it is fair to say Meta is going to compete and keep pace against a company that has >3x revenue with deep and entrenched benefits from Apple’s control of incumbent mobile computing. Only way I can see Meta to scale back materially is if Apple itself decides to exit the market if Vision Pro is a massive flop. That wouldn’t be my base case and I expect this to be protracted race between these two companies. In short, I would mostly just pay attention to Meta’s consolidated numbers.

Let’s look at some interesting comments from the earnings call:

Reels

We're seeing sustained growth in Reels and video overall as daily watch time across all video types grew over 25% year-over-year in Q4 driven by ongoing ranking improvements.

Shop Ads

Shops ads, we talked about the $2 billion annual run rate in Q4 after we just opened availability to all U.S. advertisers in Q2.

…eligible Shopify businesses can now onboard to shops on Facebook and Instagram very seamlessly. And we're making it easier for advertisers to turn their existing ads into shops ads. And we'll continue to focus on deepening integrations with partners and leveraging AI to make shops ads even more performant.

WhatsApp Channels now has 500 Mn MAU.

WhatsApp is also doing very well. And the most exciting new trend here is that it is succeeding more broadly in the United States, where there's a real appetite for a private, secure and cross-platform messaging app that everyone can use. And given the strategic importance of the U.S. and its outsized importance for revenue, this is just a huge opportunity.

Threads

Threads now has 130 Mn MAU (vs 100 mn in 3Q’23).

Open Source

For the second consecutive quarters, Zuck tried to explain to investors why Meta is taking the open source route:

One other thing that stood out to me from Zuck’s prepared remarks is Meta’s access to data regardless of how the GenAI related lawsuits will settle:

Now the next key part of our playbook is learning from unique data and feedback loops in our products. When people think about data, they typically think about the corpus that you might use to train a model upfront. And on Facebook and Instagram, there are hundreds of billions of publicly shared images and tens of billions of public videos, which we estimate is greater than the common crawl data set. And people share large numbers of public text posts and comments across our services as well.

AR/VR

“our focus for this year is going to be on growing the mobile version of Horizon as well as the VR one.”

I love my Ray-Ban Meta smart glasses, and it seems even Meta was surprised by the demand:

Ray-Ban Meta smart glasses are also off to a very strong start both in sales and engagement. Our partner, EssilorLuxottica is already planning on making more than we both expected due to high demand. Engagement and retention are also significantly higher than the first version of the glasses.

Capital Allocation

Meta bought back $6.3 Bn last quarter ($20 Bn for the full year). What was perhaps bit of a surprise was Meta has initiated a dividend of $0.5/share.

While headcount was down 22% YoY, Meta started hiring again as headcount increased by ~1k QoQ.

Opex Guide

Meta kept opex guide unchanged: $94-99 Bn. Given historical trends, investors typically expect Meta to either lower the opex guide over time or be closer to the low end of the guide. I wonder if this assumption remains relevant under Susan Li.

Capex

Capex guide range was increased from $30-35 Bn to $30-37 Bn in 2024

We expect growth will be driven by investments in servers, including both AI and non-AI hardware, and data centers as we ramp up construction on sites with our previously announced new data center architecture.

Given how well their capex ramp turned out when it was quite controversial among investors, Zuck seemed emboldened by that experience which is quite understandable:

I recently shared that by the end of this year, we'll have about 350,000 H100s and including other GPUs, that will be around 600,000, H100 equivalents of compute. We're well positioned now because of the lessons that we learned from Reels. We initially underbuilt our GPU clusters for Reels. And when we were going through that, I decided that we should build enough capacity to support both Reels and another Reels-sized AI service that we expected to emerge so we wouldn't be in that situation again.

And at the time, the decision was somewhat controversial, and we faced a lot of questions about CapEx spending, but I'm really glad that we did this. Now going forward, we think that training and operating future models will be even more compute-intensive. We don't have a clear expectation for exactly how much this will be yet, but the trend has been that state-of-the-art large language models have been trained on roughly 10x the amount of compute each year.

And our training clusters are only part of our overall infrastructure, and the rest obviously isn't growing as quickly. But overall, we're playing to win here, and I expect us to continue investing aggressively in this area. In order to build the most advanced clusters, we're also designing novel data centers and designing our own custom silicon specialized for our workloads.

In case you think Zuck has become atheist to the “efficiency” religion, he did have some reassuring words:

…we're in a place now where the business is performing well. And I think the obvious question would be, okay, well, given that, should we just invest a lot more in things?

And the biggest thing that's holding me back from doing that is that at this point, I feel like I've really come around to thinking that we operate better as a leaner company.

Even beyond 2024, my operating assumption is that we will also try to keep it relatively minimal because I think that -- until we reach a point where we're just really underwater on our ability to execute, I kind of want to keep things lean because I think that's the right thing for us to do culturally.

…a big part of why I wanted to improve our profitability is to give ourselves the ability to go through what is a somewhat unpredictable and volatile period over the next 5 or 10 years. There are different risk factors that are geopolitical or regulatory or different things, but also the technology landscape is somewhat unknown. And we want the ability to be able to surge investment on things, like building out larger training clusters or just making different investments where that's necessary.

…being a leaner company is helping us execute better and faster, and we will continue to carry these values forward as a permanent part of how we operate.

Regulation

Hard to know what to infer from the dizzying number of regulatory worries:

FTC is seeking to substantially modify our existing consent order and impose additional restrictions on our ability to operate. We are contesting this matter, but if we are unsuccessful, it would have an adverse impact on our business.

Outlook

1Q’24 topline guide is $34.5-37 Bn (+25% YoY at mid-point).

Closing Words

So, what now? The stock has become ~5x in the last 16 months. Is there really much money left on the table here? The reality is I have been listening/reading “the easy money has been made on Meta” since it went from $90 to $150. Having resisted such proclamations, I too have finally started to echo that easy money is likely indeed over.

Frankly speaking, I do not see “easy money” anywhere in my portfolio or companies in my watchlist, and it is far from clear to me that Meta is any more “difficult money” than my other portfolio holdings. I will share more thoughts on how I am thinking about it in my monthly deep dives.

My investment in Meta has been by far the most tumultuous one in my career even though it worked out more than fine so far. David Poppe’s (Giverny Capital Asset Management) recent letter had this interesting bit that really resonated with me which is perhaps also quite apt on my investment in Meta since 2018:

"The stock market is peculiar in its ability to deliver a satisfactory result over time in a manner that feels unsatisfying. It’s perhaps like a restaurant with amazing food and awful service. Or a slot machine in reverse: you mostly win and over time your wealth increases. But every so often you suffer a debilitating loss that causes real financial pain. On top of this, the losses generate headlines and the gains are often received skeptically"

For more in-depth analysis on Meta Platforms, you can read my analysis here (March, 2023).

I will cover Amazon earnings tomorrow. Thank you for reading.

If you are not a subscriber yet, please consider subscribing and sharing it with your friends.