The Economics of the Cult of Lululemon

Lululemon Athletica (Ticker: LULU) is a fantastic company. In 2005, Lulu generated $40.7 mn sales. 15 years later, its sales were ~100x of that, implying an astounding ~35% CAGR over this period which was almost entirely organic in nature. For context, Amazon grew at ~28% CAGR during the same period. Talk about product-market fit!

Let me pour some cold water to your excitement after reading the first paragraph. I am not bullish on Lulu, the stock, right now.

In this deep dive, I will first discuss why Lulu has been such a successful company at a time when we are writing obituaries of so many other retailers. I will then dive deep into the numbers to explain the business in more detail which will be followed by valuation discussion. Finally, I will discuss some optionality which may make my current bearish tone shortsighted if this optionality goes in Lulu’s favor in a major way.

Understanding the Cult of Lulu

In 1998, Chip Wilson founded Lululemon in Vancouver, Canada. While attending in one of the Yoga classes during ‘90s, he noticed women in his class were wearing transparent and thin dance clothes which were “shrunken version of men’s sweatshirts and t-shirts”. He wanted to give women a better clothing option and voila, yoga pants and Lululemon were born.

By any measure, Lulu’s yoga pants were a revolution in how women dress in the West. While it was originally intended for yoga classes, it soon went above and beyond this narrow use case and became quite pervasive. In an era when fast fashion has taken over the rest of the retail, Lulu’s pants proved much more durable.

I listened to the audiobook “Little Black Stretchy Pants”, written by Chip Wilson, to understand Lulu’s incredible success. I really enjoyed the book and it helped me understand how Lulu is unique. There are lots of interesting nuggets in the book that I am tempted to mention, but since this is a deep dive, and not a book review post, I will rein myself in. The book, as well as recent analyst day, 10-k, and earnings transcripts, led me to believe that there are primarily four factors that were behind the rise of Lululemon: innovation, brand, distribution, and marketing. I know these sound pretty generic rationales, so let me elaborate on each of the points.

Innovation: Lulu, for all intents and purposes, invented the “Athleisure” segment, a term that is actually not endorsed by Mr. Wilson. He prefers the term “technical apparel” as he explained why he doesn’t like the term “Athleisure”, “That’s the last thing in the world that it is — leisure. We come from function first and then make it look good, where athleisure is looking good and then trying to make it look athletic.”

Lulu’s culture of innovation stems from its founder as he obsessed over how he can make Lulu’s success enduring in an industry in which most successes are largely ephemeral in nature. Wilson mentioned in his book, "Each day I walked into the office and asked myself, 'If I had to compete against Lululemon, what would I do?...I was fanatical about building a moat around our success.”

So, what’s so special about those yoga pants?

To find out, I ordered online a pair for my wife. Now please note that MBI household does not like to splurge $100 on a pair of pants as it clearly violates my sense of “value”, but I had to order anyway in the name of “research”.

It turns out these yoga pants are “extremely comfortable” (quoting from the horse’s mouth). I spoke with a number of women and it’s the first thing they all said to me. More importantly, this comfort does not come at the expense of your sense of fashion. One friend mentioned how yoga pants also accentuate female body. A competing women’s pants brand named “Spanx” literally have a segment called “Booty Boost Active”. The juxtaposition of comfort and fashion is indeed the holy grail.

To protect the IP, Lulu patented the materials known as “Luon” by which these pants are manufactured. Luon is basically 81% nylon and 19% lycra. Considering the success of yoga pants, competing brands have come up with their own lines of yoga pants. Athleta, a GAP brand, had introduced its yoga pants which typically costs ~$20 less than Lulu’s. Athleta patented its own material called “Pilayo”, which is 88% nylon and 12% lycra. Nike, Under Armour, Reebok all introduced their branded yoga pants as well. Historically, Lulu had been aggressive in trying to protect IP, but it eventually either settled or dropped the charges altogether.

As much as Lulu wants me to believe the superior technical performance of its products, I think this is the famous Coke/Pepsi/RC Cola problem. I wonder how many women would really be able to differentiate a lulu pant from an Athleta pant if we remove the logos. Therefore, even though Lulu would indeed get high marks on innovating, educating, and revolutionizing how women dress in the West (and increasingly in Europe and South East Asia), innovation itself was perhaps not the reason for its continued success which is a good segue to the three more important reasons for its durable rise: brands, distribution, and marketing.

Brand: While we all probably understand what a “brand” is, I recently came across a definition that really resonated with me. Patrick O’Shaughnessy in a recent “Acquired” podcast episode mentioned how he thinks about brands: a brand is “just high quality, low variance outcomes…Can you just consistently deliver something really high quality so that you build trust with people. Trust takes time, therefore it takes consistency”

That’s a very interesting way to look at brands and the more I thought about it in different contexts, it made intuitive sense to me. “MBI Deep Dives” also tries to accomplish exactly that: high quality, low variance of investment research.

Let me explain how Lulu fits into this context. Lulu’s products are certainly high quality. Lulu has only 39 vendors worldwide (mostly in Vietnam and Cambodia) that manufacture their products, and just five of them produce 56% of the products. The largest manufacturer produced 17% of the products in 2019. So, Lulu clearly runs a tight ship which helps them maintain consistent and high quality of the products. This strategy clearly has a trade-off as Lulu develops a significant co-dependency compared to a more diversified base of manufacturers.

Why is maintaining such high quality of the products so important? Stuart Haselden, former COO of Lulu mentioned in 4Q’18 earnings call, “Our return rates, in particular, are very low, which helps explain why we enjoy a better rate -- margin rate online than other companies.” This is of paramount importance because return rates in apparel online retail is 3x higher than stores. Consistent quality is not the only reason for Lulu’s low returns, but it certainly helps.

While Lulu gets high marks through broad lens on brands, it still does not capture the full essence of the power of its brand. Some brands confer some “badge value” that sit on top of the broader definition of “high quality, low variance” of brands. Owning a “Ferrari”, for example, provides a clear signal of your net worth. While Lulu pants cannot possibly have the same signaling effect as a Ferrari does, it most certainly signals that you were willing to forego a $20 yoga pants from Amazon or $79 ones from Athleta. The “badge value” of Lulu logo has a social signaling power which appears to be expensive if you think you are buying yoga pants but can actually be a very “cheap” way to express your fashion sense, taste, and social status. This status symbol perhaps becomes even more prominent in international markets as Lulu’s products cost similar across geographies.

While Lulu’s logo has its power, brands are likely to be less durable moat compared to moats such as network effects. Lulu’s rise was amplified by its marketing, and distribution strategy which may help them sustain its brand for a long time.

Marketing: The first question that popped in my mind while looking at Lulu is how the hell Nike cannot outcompete Lulu. I have always thought Nike has an incredible durable moat not only because of its brand but also how the brand can consistently reinforce its message because of its scale. In essence, when I think about Nike, I don’t think of them as a company selling sneakers and shoes. They are essentially a marketing company that just happens to sell shoes.

Nike spent $3.6 Bn in advertising and promotion last year which is ~10% of its revenue, but almost close to Lulu’s entire topline. Nike’s biggest differentiation from Adidas/Under Armour is not necessarily better-quality shoes but its ability to get the endorsement from the biggest superstars in the world. If you are competing against Nike with Nike’s own playbook, it is difficult to see how you can consistently win. It is difficult to match Nike’s endorsement deal numbers without destroying your margins in the process. For context, Adidas and Under Armour (UAA) generates ~70% and ~15% of Nike’s revenues respectively.

Lulu understood the vulnerability of such lopsided game from the very beginning and opted for a marketing strategy that is more community driven.

Lulu has currently more than 2,000 ambassadors in the world. A typical ambassador is two-year journey with the brand. Apart from the current ambassadors, Lulu also has 15,000 legacy ambassadors with whom it also maintains and nurtures the relationships.

So, who are the typical ambassadors? Of the >2,000 ambassadors, fewer than 50 are considered global ambassadors, most of whom are athletes of different sports (none with global mass appeal). The vast majority of the ambassadors are considered “store ambassadors”. Most store ambassadors are typically local yoga instructors or fitness experts. But anyone with some social influence can apply to Lulu’s store ambassador program.

What do they have to do once they become ambassadors? The ambassadors are essentially the spokesperson of Lulu to their respective communities. They can arrange free in-store yoga classes or a series of in-store monthly discussions on topics of varied interests depending on the ambassador.

What does Lulu have to do for their ambassadors? Well, not much. The store ambassadors get early access to new products and events. Lulu listens to the ambassadors’ feedback and some can be part of their design and product decisions. It is basically a symbiotic relationship between ambassadors and Lulu as the ambassadors get a chance to grow their business by meeting new people and potential customers in a Lulu store. Lulu, on the other hand, gets a quasi-third person to promote its products to its customers which feel much more authentic and genuine than a random superstar who clearly gets a gazillion of dollars to tell you to wear a particular branded shoe. Given Lulu’s clout, I imagine these ambassadors are indeed genuine fans of the brand themselves which makes the connection with their customers stronger and a lot less transactional.

What I really love about these store-ambassador led in-store activity is it provides a sense of purpose to Lulu’s brick-and-mortar store base beyond being just another shopping place. In physical stores, foot traffic is the ultimate barometer, and making their stores a focal point for these in-store activities/programs and utilizing ambassadors effectively to engage and integrate customers to the Lulu fandom is something that is very very difficult to copy by the competitors. It is also far cheaper and arguably more effective than using mega stars as your spokesperson. The economics of the super star endorsements is unlikely to improve going forward given their pivotal role in branding as well as the marketing dollar that are chasing them. Lulu has so far largely escaped this rat race altogether.

The numbers depict the effectiveness of Lulu’s strategy. Lulu’s retention rate of its high value customers, defined as top 20% customers, is 92%. It also enjoys NPS of 83. These staggering numbers clearly substantiate the aura of Lulu among its ~7 million customer base.

Distribution: Lulu is a vertically integrated retailer. In layman’s terms, unlike Nike/Adidas/Under Armour, you cannot buy Lululemon products from your nearest Footlocker or Dicks store. You need to go to either a Lulu store or order directly online.

Lulu cares about controlling the customer experience as you simply cannot outsource to someone else to build and maintain a cult following of your brand. Lulu’s real estate strategy caters perfectly to such cult following.

There are four types of Lululemon stores:

a) Traditional stores: These are typically 3,000 sqft stores. 5/6 years ago, this was the only kind of store Lulu had regardless of whether the store was in a suburban market or a downtown hip neighborhood.

b) Seasonal stores: Lulu signs three to six months of short leases and opens 60-70 seasonal or pop-up shops each year. They do this at times to test the water before coming up with full-sized stores or sometimes it can be just because the market/location in question doesn’t make a lot of economic sense to build a full-sized store but can still be lucrative in generating foot traffic and capitalizing on the local demand in a seasonal smaller store. In fact, on an average, 35% of all customers in these stores are new customers, and management mentioned these stores typically over-index the traditional stores.

c) Co-locating store: this is basically transforming some of the current store base by extending sqft size from 3,000 to 5,500 sqft. The expanded store allows to have both men’s and women’s product assortments in the same store. Lulu mentioned after expanding the store size and including men’s merchandises more, their men’s business in these stores grew 50-60% in year 1 without any additional breadth of assortments. Even after year 1, these stores typically comp higher than traditional stores. Lulu initially wanted to have separate men and women stores, but they are leaning more to co-locating strategy to drive growth.

d) Experiential Stores: These are 20,000 sqft giant stores, like the one in Lincoln park, Chicago. This not only consists of a typical store but also has meditation space, two “sweat studios” which offer 6-10 classes per day, and includes “fuel space” offering coffee, juice, smoothies etc. The walls of the Lincoln park store are decorated with 45 ambassadors of Lulu. By 2023, Lulu expects ~10% of the store footprint will be “experiential stores”.

Lulu’s real estate strategy makes it clear they do not have one-size fits all approach and understands the degree of differentiation required to make your physical store footprint standout from all the commoditized nature of store base out there. As mentioned earlier, what really impressed me is that their physical stores have a clear sense of purpose and how it is centered around building, nurturing, and elevating the experience of being part of the Lulu cult. Last year, its sales per square fit was $1,657 compared to an average of ~$325 in the US retail, substantiating just how successful Lulu’s strategy has been.

Of course, all 7 million customers not necessarily feel they are part of the “cult”. Many of them just presumably want to have a nice, comfortable, and fashionable pants that they can wear seemingly everywhere. They may not necessarily want to come to the store to attend the sessions with the store ambassadors. Even for them, Lulu’s Direct-To-Consumer (DTC) strategy ensures Lulu gets to capitalize on such customers.

Chip Wilson mentioned why he never wanted to pursue wholesale retailing, and always preferred vertical retailing concept. Some of his primary rationales include the ability to control the brand, and not markdown products to boost sales which can obviously dilute the brand. The other rationale that he mentioned was very interesting. He explained in the wholesale model the retailers just want the brand to keep sending them what have sold well in the past. It is difficult to innovate and take risks with new designs/fashions under the wholesale model.

But Chip wanted to “design from amnesia”. A desire for continuous innovation with a “hedgehog” like mindset was only possible in a vertical retailing model. One might wonder if vertical retailing makes so much sense, why don’t other companies do it? Well, it’s a lot more capital intensive to build your store footprint, logistically more difficult, and takes a lot more time to scale. But category leaders are more and more appreciating vertical retailing as Nike has also started focusing on DTC.

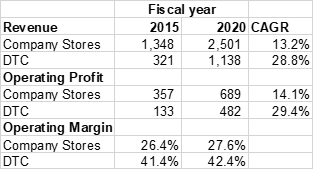

In the last few years, Lulu has been a direct beneficiary of the secular trends such as e-commerce and DTC. 5 years ago, DTC was 17.9% of total sales. When other retailers are pondering whether shifting to e-commerce is going to cannibalize their both top and bottom line, just look at the below table to see what Lulu has achieved in the meantime. Both topline and bottom line of store sales and DTC sales grew at an envious rate without sacrificing margins.

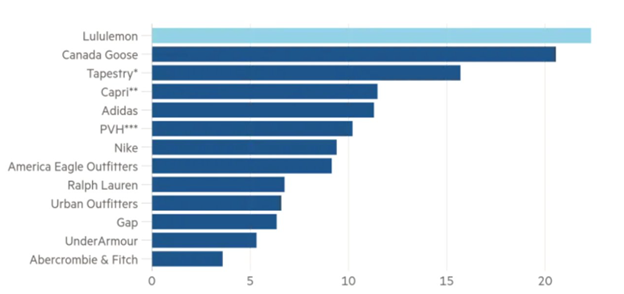

While the business models are not exactly the same, the profitability difference among the retailers further substantiates that Lulu is operating in a different league.

I should also note that the work culture Lulu had built over the years also likely to have played a role of paramount importance for its success. As per the Lulu lingo, customers are called “guests”, and salespersons are known as “educators”. According to Glassdoor, 89% (vs 84% for Apple, 77% for Amazon) would recommend the company to a friend. The founder Chip Wilson did recognize employees are not just a means to an end, but real people who resonate much better with their work when their holistic self are also taken care of. From its formative days, Lulu employees were told to write their goals for the next 1, 5, and 10 years out in three aspects of their lives: personal, career, and health. Of course, many companies can come up with these fluffy strategies, but to execute it, and convince the employees to take it seriously and believe it earnestly is a different ballgame.

Okay, enough adulation of Lulu. The rest of this deep dive will be a lot more critical than it has been so far which will also clarify why despite all these, I am not pulling the trigger just yet.

Valuation

If this is the first time you are reading my deep dive, I strongly suggest you read this post first to understand my approach to valuation. I will not spend much time here explaining my valuation approach and for a first-time reader, it would be a good idea to read my valuation approach post first, and then come back to this deep dive.

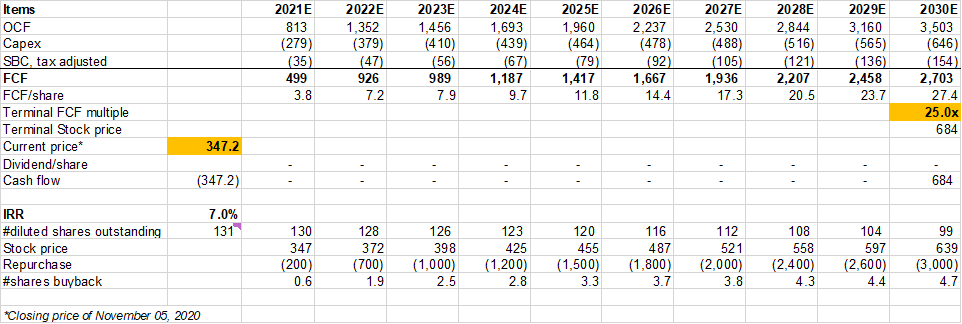

Let me do this a little backward. Before explaining the drivers in the model, let me show you the output first. In my model, I was trying to generate ~7% IRR, and to do that, I made certain assumptions which I will discuss in much more detail below. In the terminal year, I used 25x FCF multiple to generate ~7% IRR from the current stock price. Is 25x multiple a little too high? I would agree that it is a little too high, but I will come back to it later. I just wanted to show you the output first before delving into the weeds. As always, instead of treating this model as gospel, I strongly encourage you to download the model and incorporate your own assumptions as you see fit.

Delving into the details of the model

(Update June 15, 2021: Please note that I have posted my updated thoughts on Lululemon here. For the sake of transparency, I am still keeping my earlier thoughts on Lululemon valuation on this deep dive.)

The model shown below has 10 years of historical data and 10 years of projections to do the reverse DCF analysis. Let’s start with the topline.

Revenue

Lulu discloses revenue by channel, geography, and gender. For the purpose of building the model, I will primarily focus on revenue segment by channel, but will briefly touch upon on other ways of segmenting revenues as well.

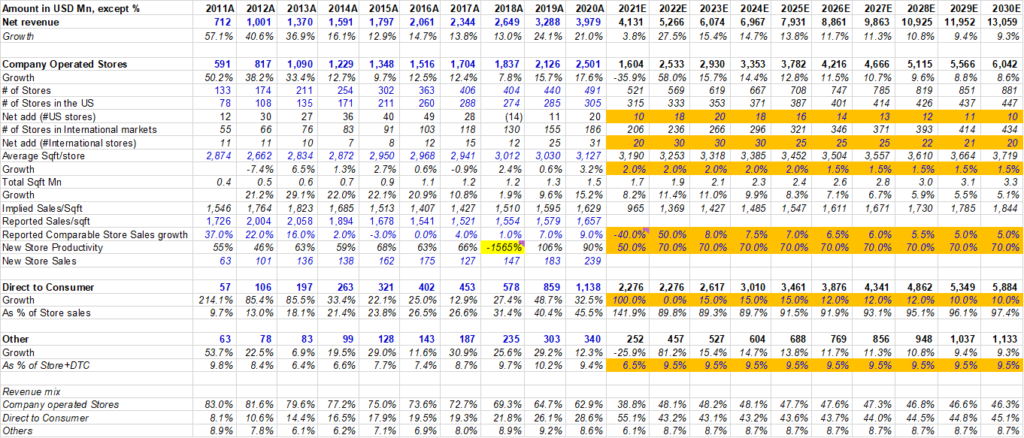

When disclosed by channel, Lulu segments revenue in three ways: Company operated stores, Direct to Consumer (DTC), and Other. Please note that Lulu’s fiscal year ends in January, not December. Therefore, 2021E indicates current fiscal year, not the next one.

Lulu started as a yoga related brand, and given that ~72% of yoga practitioners are women, Lulu was a huge hit with women. Yoga was a robust secular tailwind for Lulu as yoga practitioners increased from 15 mn in 2008 to 36 mn in 2016 and ~55 mn in 2020 which means currently 2 in 5 women from age 15 to 64 practice Yoga in the US. Number of men practicing Yoga increased from 4 mn in 2012 to 10 mn in 2016. Perhaps just the secular trend of Yoga itself was a significant contributor to Lulu’s success.

In the last 10 years, Lulu’s revenue increased by 5.6x (21.1% CAGR). Such remarkable growth was driven not just by DTC (39.4% CAGR), but also by company operated stores (17.4% CAGR).

Company Operated Stores: Revenues from company operated stores are driven by number of store openings, square feet growth, and most importantly, Same Store Sales (SSS) growth. As of 2Q’20, Lulu has 506 stores. New store opening plans as well as sales in existing stores have understandably been affected by the pandemic. In 2019 analyst day, Lulu mentioned they expect to see low double-digit square footage growth in its stores channel in 2019-2023. Despite the temporary hiccups during Covid-19, my projections assume Lulu will meet that target.

Same store sales were choppy between 2014 and 2018, but the new CEO Calvin McDonald really turned things around in the last two years. Because of the pandemic and stores being closed, Lulu stopped reporting SSS numbers in the current fiscal year, so I assumed the SSS growth in a way that appears to match with the overall number. I assumed a major pick up (+50% growth) in SSS in fiscal 2022 and then assumed a mid to high single digit growth after that. Considering the historical choppiness, the future implies almost near-perfect strong execution.

Let me discuss some of the reasons for the historical choppiness. In 2014 fiscal year, a manufacturing error led the company to recall 17% of its pants inventory from stores which caused $60 mn revenue impact in that year. Two years later, there was another product recall, albeit at a much smaller scale, of 300k hooded tops. Since then, Lulu has tightened its supply chain and quality control further, but of course such idiosyncratic events and resultant choppiness are always a possibility, especially in vertical retailing business. It will certainly not be easy to post such steady mid to high single digit same store sales growth for the next 10 years.

I will elaborate on the DTC business, and then discuss the drivers of Lulu’s growth runway.

Direct-to-Consumer (DTC): DTC is basically Lulu’s e-commerce channel which has grown from just 8.1% of total revenue in 2011 to 28.6% in 2020. Of course, during the pandemic, digital penetration in the business has risen dramatically and as of 2Q’20, DTC was a whopping 58.3% of total revenue. Forecasting DTC sales following the pandemic is quite tricky.

Prior to pandemic, Lulu was trading at ~$260/share. After the Armageddon scenario was eliminated, just like the market it not only roared back but also reached a new high of almost $400/share, a whopping ~50% higher than pre-Covid. Therefore, the message is clear from the market. The pandemic is extremely positive for Lulu. I am not so sure, and even though shift to DTC is margin accretive for Lulu, I would actually argue that the pandemic could be a net negative for Lulu if stores lose relevance to the Lulu story.

Lulu is not a pure-play e-commerce player. Although its DTC business almost doubled in 2021 fiscal year so far, overall revenue declined 6.6% in the first two quarters because of the store closure and acute lack of productivity even when they were re-opened. The revenue decline clearly indicates that while most sales just moved from stores to online, overall market did not expand for Lulu.

For Lulu, I think it was just a pull-forward of digital penetration that was already underway. But following the pandemic when stores open again and come back to normal productivity, wouldn’t most of these customers go to store again? Its store base is a fixed cost, and the leases are obviously long-term in nature (weighted avg remaining lease term ~6 years). I believe it is in Lulu’s interest that their stores maintain a sense of purpose.

Competing against Lulu online might be easier for other DTC brands out there but competing against Lulu which has an incredible community base with regular store-based activities and seamless omnichannel experience is much more difficult. Maintaining the same level of passion for the brand and a sense of community might be much more cumbersome over digital channel.

If the pandemic’s impact greatly subsides soon, I would be surprised if the DTC segment grows at all in the next fiscal year. In fact, it would be pretty impressive if they somehow maintain this year’s DTC sales next year. Even if the DTC sales remain the same next year, it implies 40% CAGR from 2019 DTC sales whereas it was growing at 30% CAGR in 2014-2019.

In a no-pandemic scenario, it looks optimistic to assume Lulu will not see its DTC business decline next year. Again, the current year’s revenue numbers don’t indicate Lulu’s potential market size dramatically increased because of the pandemic; the sales mostly just shifted channel from stores to online.

Beyond the short-term, I have some long-term concerns as well looking at the embedded expectations in long-term topline growth rates.

In its 2019 April Analyst Day, Lulu identified three key growth drivers: Men, International, and Digital. Management guided that they expect sales from men’s products and digital channel to become 2x and international sales to 4x by 2023 (base year 2019 fiscal year). My reverse DCF model implies digital to be 3x of 2019 DTC sales in 2023, and since I do not model men’s or international revenues separately, let me add some qualitative discussion around those segments.

Nike and Lulu have the opposite challenge. While Nike is the undisputed king in Men’s sweat activities, Lulu dominates the sweat life of women. Now they both want to protect their turfs and then encroach into the other’s territory. Although I have not done any deep dive analysis on Nike yet, so far it looks like Lulu has been doing a better job at luring men to their brands than Nike attracting women to their brand.

Lulu’s recent success so far with men has been somewhat surprising. Lulu started as a brand largely associated with women’s yoga pants and it has certainly become an iconic brand for women. In fact, when Lulu started focusing on men as well, there were quite a few reports (see here and here) on how men were not comfortable with the logo being prominently displayed on their attire. Lulu finally listened to those complaints.

Given that I have not personally used Lulu’s products, I went to their website and started looking at men’s section. To my surprise, I could not find their logo on any of their products displayed although I could easily see the logo prominently placed on women’s products. Then I went to their separate social media channel for men (see here) and yet could not see the Lulu logo. I found it strange that if you want to pay premium for the brand (yes, it’s just as expensive for men too), why would you want to not display the logo?

I found it hard to believe, so I reached out to a friend of mine who have used Lulu’s men’s products. He confirmed that Lulu does use its logo on all of its products, but it is very discreet on men’s. I asked whether people can tell if you are wearing Lulu. He said if you know where to look, you can tell, but it’s definitely not as prominent as Nike’s logo. He further mentioned that while he prefers to wear Nike while working out, he wears his Lulu for going out. He said he cannot quite explain the aura of Lulu but agreed that it’s comfortable and product quality is pretty good.

I mention these interactions because I still remain unconvinced about Lulu’s continued success with men. I wonder whether the recent faster growth trajectory is just a low base effect as Nike’s revenue from Men is ~17x of Lulu’s. A part of the success could also be explained by a re-arrangement of the real estate strategy. Lulu used to have separate stores for men and women, and they recently started building more “co-locating” stores (described earlier). Another contributing factor is the rise of men’s interest in Yoga.

Many of the driving forces for Lulu’s success among women is conspicuously absent in its men’s segment. While brand and the Lulu logo is evidently a powerful theme for women, it seems like both Lulu and the men would prefer to hide the logo, a bit strange for an expensive pair of shorts, t-shirts or hoodies. The sense of community is also largely absent among men. In fact, Lulu seems more interested in following the traditional playbook of marketing when it comes to men’s segment. In 2019, Lulu signed Nick Foles, the 2018 Super Bowl MVP, to be its Global Ambassador. It was Lulu’s first relationship with an NFL player, and it seems to be the typical Nike/Adidas strategy rather than Lulu’s signature community-based marketing. I am not convinced Lulu can be a long-term winner in this segment by playing the game in Nike/Adidas’ terms.

Now let’s talk about Lulu’s presence in international markets.

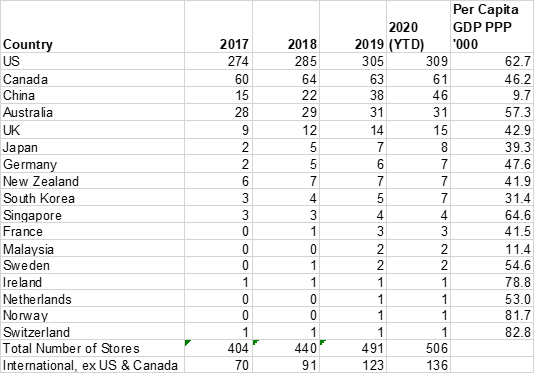

Lulu has its stores in 17 countries in the world, and only in 9 of those countries, it has more than 5 stores. Looking at the below table, markets such as Canada, Australia, New Zealand, Singapore, Ireland appears somewhat mature market as number of stores opening hasn’t grown much over the last three and half years. Some may look at Lulu’s stores and compare with other major brands’ retail presence and conclude there is a huge growth runway left for Lulu in international markets. But of course, the people who are willing to spend $100 for a pair of leggings in international markets may not be too big either. It is, however, possible that Lulu can become an exciting brand just for the affluent class in the international markets.

I wonder whether Lulu’s community-based marketing strategies can hinder them from scaling faster in international markets. Nike, by signing Cristiano Ronaldo, can make the Nike brand seem appealing to billions of people in the world. There is a reason Ronaldo gets to sign $1 Bn contract with Nike. But if Lulu tries to play the same game, it will provide mixed signal to the broader community-based strategy and as mentioned earlier, I don’t think Lulu can win by playing the game in Nike’s terms.

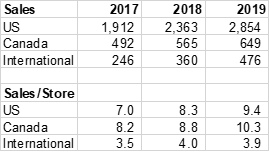

My reservation with international markets also comes from not so exciting economics abroad. Below I show the sales per store (revenue divided by current year number of stores) in the US, Canada, and in international markets. This is bit of a flawed comparison for two reasons: I am assuming similar size of the store across geographies which may not be the case, and since net new stores are opening faster in the international markets, sales per store may appear much lower than it actually is on an apple-to-apple comparison. While I do not know whether the stores’ size is materially different across geographies, I did try to amend the second flaw in this measure. Instead of dividing revenue by number of stores, I tried to divide current year’s revenue by previous year’s number of stores which is also flawed since obviously new stores opened generated some sales. Even in this measure, international stores generated ~$5 mn sales/store (instead of ~$4 mn, as shown below, when dividing sales by end of year number of stores), almost half of what stores in the US and Canada are generating. I will further discuss margins in international markets shortly.

It is clear that Lulu management sees more opportunities in Asia than they do in Europe, and the pace of new store openings certainly reflects that understanding. Here’s what Lulu’s VP of International segment told analysts in 2019:

“I think, fundamentally, the market dynamics are very different. There is just a more robust appetite for, I think, western brands generally in Asia. And there is a growing health and fitness trend in China supported by the Chinese government, specifically, that is helping sort of add to the tailwind for businesses that participate in those markets. Those factors don't exist in the same way in Europe. We had some painful lessons in Europe where we did abandon, in certain cases, our proven showroom model, open stores in locations based on attractive real estate where we hadn't yet adequately developed demand, brand awareness in the community in those markets.”

In the last analyst day, Lulu management also unveiled some plans to expand the brand to some adjacent areas. Lulu has already made some inroads beyond yoga pants and some of its design of women’s bras became quite popular. Lulu even mentioned that “And at some point in the future, we boldly feel that our bras will be as big as our pants.”

If women’s bra segment indeed becomes as big as pants, it can possibly support the growth implied in the model. Given Victoria’s Secret’s struggle, there can be some opportunities for Lulu to grow this segment. But these segments are notoriously difficult to pick winners. Beyond women’s bra segment, Lulu outlined some longer-term ambitions into Selfcare segment. It includes products such as deodorant, dry shampoo, lip balm, facial moisturizer etc. Success, of course, is far from guaranteed in these adjacent markets.

Management also emphasized that their 2023 targets do not depend much on penetrating the adjacent markets, but rather on leveraging the core markets. While management guided revenue growth of low teens between 2018 and 2023, my reverse DCF implies 16.6% topline CAGR between 2018 and 2023. Between from 2023 to 2030, the implied topline CAGR is 11.6%. Therefore, market certainly expects the growth runway to be fairly long and will continue for the entire decade for Lulu.

Great companies do tend to surprise not just investors and analysts, they routinely surprise management too. So, I am not claiming that this is not achievable by any means for Lulu; perhaps they will also be incredibly successful at women’s bra segment as well as some of the adjacent markets. Looking at the embedded expectation, it does seem Lulu is enjoying some sort of cult premium in expected long-term growth rates. Personally, I think this is likely to prove too lofty to match even by companies as great as Lulu.

Cost structure and profitability:

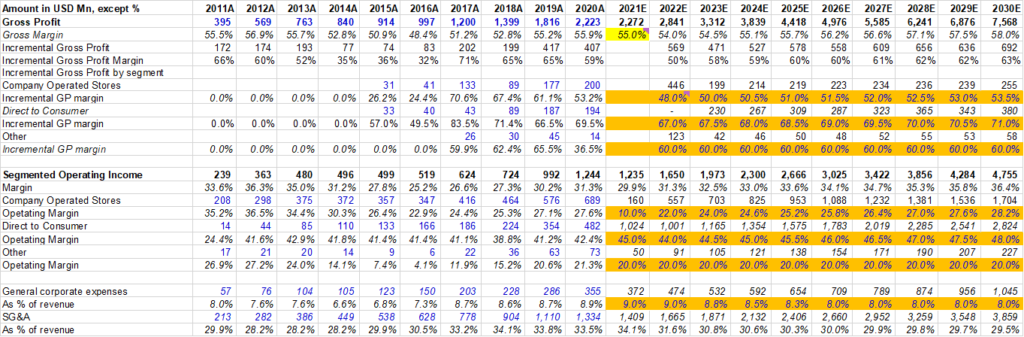

Management guided that their 2023 plan to achieve mid-teen earnings growth assumes modest gross margin expansion and modest SG&A leverage.

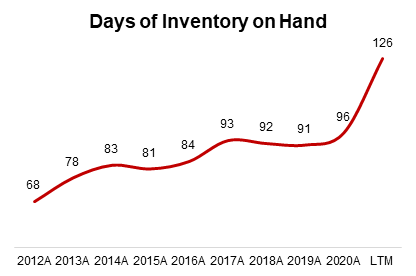

Most retailers attempt to expand gross margins by trying to reduce markdowns. While Lulu has a section called “We Made Too Much” (WMTM) on its website, markdowns are lower percentage of the business compared to other retailers. Lulu has improved its gross margins by over 700 bps by streamlining supply chain and closely partnering with selective vendors, but the path forward to further margin expansion is likely to be much more challenging. Just look at the LTM Days of Inventory on Hand (DOH). During this pandemic, Lulu’s DOH has increased by a whopping one month in last twelve months. Holding inventory longer is obviously bad news for margins, and the jury is out there how long it will take for them to normalize DOH.

I would have loved to do a bit more granular level analysis on margin by each segment. Unfortunately, while Lulu publishes incremental gross profit data, it does not disclose gross margin by segment. It also does not disclose breakdown of SG&A expenses. Therefore, the opportunity to be creative and build a deeper understanding of the business segments as an analyst is somewhat limited given the lack of disclosure.

Long-term margin expansion opportunities may depend on Lulu’s ability to drive better profitability in the international markets. There are some ambiguities when it comes to margin prospects in the international markets. At one hand, international markets such as China over-indexes on DTC which is higher margin business, but management also pointed out international is going to be structurally not as profitable as North America business is:

“The cost structure challenges in our international markets and in China, specifically, fall into a few different areas. As you look at a 4-wall store cost profile, rent and labor cost more. And that is just a fact versus North America. As you look below that, to the overhead operating costs, we have made important investments in the team and the capabilities regionally. And part of what we're now seeing in terms of reaching profitability is the economies of scale as the business grows and we're able to leverage those investments.

…there are some fundamental elements of operating overseas that, in the cross-border costs, from an inventory standpoint, are all real. And the comment that I offered in the presentation that we see that improving but likely will be structurally lower than North America is how we wind this up.

…It will likely always be disadvantaged due to certain structural cross-border costs versus North America, but we can close that gap significantly and we will.”

It is difficult to tell what extent these gaps can be closed, and where the debate will be settled. Given the lack of disclosure on margin level data in the international markets, it is bit of a guessing game at the moment. I am, frankly speaking, a bit puzzled to read this comment from management and I am not sure I quite understand the point about structural differences that will make International markets, especially China inherently less profitable compared to North America. If any of you reading this piece has a better understanding on this point, feel free to drop me a message. As you can see below, the model implies ~500 bps operating margin expansion. As channel shifts from stores to DTC, margin is indeed likely to expand, but how well Lulu can improve margins in the international store base is not easy to build conviction on.

Two optionalities: membership programs and Mirror acquisition

If you are a Lulu shareholder, you are perhaps really excited about the potential of these two optionalities. Let me discuss these two optionalities separately.

Membership Programs

In 2018, Lulu ran a pilot for Membership Program in Edmonton and Denver. It was $148/year (or $128 CAD/year) during the pilot. The price has been increased to $168/year in 2020 and the program has now been expanded to Toronto, Chicago, and Boulder.

What do the members get? A Lulu member will get one welcome free product (typically a pair of Align pants), an annual wellness membership which allows members to use the pass once every month to attend participating fitness/yoga studios, enjoy 20% discount (up to 10 items) on shopping around the member’s birthday week, get early access to products, and personal development content.

At first, I was trying to understand the economics of the membership program from the company’s perspective, and it then occurred to me it is perhaps not the right way to look at such a program. I believe the economics of the subscription program should always start from the customer’s perspective.

Netflix’s monthly subscription plans or Amazon Prime’s annual plans wouldn’t make much sense if you just think from company’s perspective when they were launched. But boy oh boy, they felt like such a steal from a customer’s perspective, and when millions of customers felt the same, it started to make sense for the companies too.

Customers are not stupid; they can do the math. That’s why I think the most important thing for this membership program is: what does a customer see when she comes across this program and how does she evaluate the attractiveness of the offer?

Here’s what a Lulu customer sees in this membership program. She gets a free product which retails at $98. She gets to attend Yoga/fitness studios which retail at $20-25 price point. While she’s probably unlikely to attend all 12 classes, she expects to attend at least 3-4 classes, so that’s another $60-80 of value. On her birthday, since it’s discount week, she may just buy 3-4 pairs of her favorite Lulu pants that will last the rest of the year. That’s another $60-80 of value. And then there are some intangible benefits such as access to early Lulu collection which although hard to quantify can certainly lead to some social brownie points.

So, if you add it all up, it’s ~$250+ some intangible personal/social benefits at the price of $168/year. Hmm, not bad.

If I were a regular Lulu customer, I would probably conclude it makes sense to be a member. Now let’s change gears and think from the company’s perspective.

Let’s assume this membership program is available for anyone to join, not just those specific locations it is available now. Lulu mentioned in 2019 analyst day it had more than 7 million guests in 2019 fiscal year. Assuming 7 million guests, based on 2019 fiscal year sales this implies $470 sales per guest per year. Lulu also reported that it has 92% retention rate among its top 20% guests. Considering Lulu’s cult following, let’s assume the top 20% customers i.e. 1.4 million people will join the membership program when it is available for everyone. Given the average customer spends $470/year, I would imagine these top 20% customers spend $1,000 or higher on Lulu every year. Assuming ~$100 for an average item bought on Lulu, this implies these customers buy ~10 items every year from Lulu.

So, what happens when they join this membership program? They pay $168/year. They get a welcome gift worth ~$100. If these cult-like customers decide to buy 4 items on their birthday week, Lulu doesn’t make money from membership program. The real question is whether these customers will buy more from Lulu than they did once they become Lulu “member”. If instead of 10 items they buy 12 or 15 items per year from Lulu, the discount they receive on birthday or free welcome kit may not be cannibalizing compared to if they don’t increase purchase volume at all.

I do not know answer to this question, and I doubt many people know either. In fact, the whole idea of a pilot and gradually launching this to other locations is to gather data points and test these sensitivities. And the fact that Lulu has increased the price point from $148 to $168 in less than two years perhaps indicates the management did not think the economics of the program was compelling enough at the previous price point. If that continues to be the case even at $168 in the current iteration, it is possible Lulu might even close the membership program altogether.

I believe the success of this subscription plan depends on Lulu’s ability to generate demand for this program from casual customers, not the cult customers. During the pilot, Lulu was able to attract ~10-13% new customers i.e. who bought Lulu for the first time to sign up for the membership program. In fact, management mentioned during the first four weeks of the pilot in Edmonton, Lulu sold twice as many memberships as its best-selling yoga pant in that area. Therefore, it is possible that this program will transform a lot of casual and new Lulu customers into an entrenched Lulu customer. It is still too early to predict success or failure as these data may not be representative of overall customers.

If Lulu attracts a lot of new customers through this program and # of items bought on birthday discount week comes down to 1 or below, the contribution margin (defined as revenue-welcome gift-discount divided by revenue) increases to ~30%. Please note that I did not consider all the expenses of operating the membership program since we do not have much data related to this. It was an attempt to get a basic sense of the economics of the program. If we consider all other variable and fixed expenses related to the program, the actual margins will probably be even lower.

Under the current business model, Lulu already enjoys ~30% operating margin. Therefore, even under a possible best-case scenario, if all we can achieve is ~30% contribution margin, do we really need this membership program and what “value” can we assign based on current information? Not much I think.

To play devil’s advocate, the beauty of annual subscription program is the recurring and upfront nature of the cash flow which was not fully captured in this basic analysis. Plus the possibility of attracting new customers and hence reaching a better scale can outweigh short-term margin sacrifices. Overall, considering all these uncertainties, I would not assign too much value on this program as it stands now. I would wait and see how things progress.

Mirror Acquisition

On June 29, Lulu announced that it would acquire home fitness company Mirror. Before the announcement, the stock closed at $294/share on that day. Two months later following the Mirror acquisition, on September 2nd, the stock was trading at almost $400/share. Lulu bought Mirror for $500 million. The market cap Lulu added in just two months after acquiring Mirror was ~$14 Billion. Please note there was no other major announcement/earnings call during this period and hence presumably Mr. Market was attributing a lion’s share of the market cap increase to Mirror acquisition. Before labeling the whole episode as nonsensical, let’s dive deep into Mirror first.

What is Mirror? Founded in 2016 and launched in September 2018 by a former Lululemon ambassador named Brynn Putnam, Mirror caters to at-home fitness studio experiences that combine both a screen and a mirror that hangs on a wall to deliver live and on-demand content ranging from boxing to yoga and meditation while simultaneously allowing the user to see their physical form. If you have no idea what I am talking about, watch this YouTube video explaining what Mirror is.

A mirror, the hardware, costs $1,495. To attend the on-demand or live fitness classes, you need to subscribe to the Mirror mobile app for $39/month. Therefore, it’s not just another one-off hardware sales, but generates a steady, recurring subscription-based cash flow.

What’s the management’s case for Mirror acquisition? Lulu initially invested in Mirror back in mid-2019, and they had an inside view of Mirror through that investment before fully acquiring it. This set up makes me feel this is a much more informed transaction than a typical M&A deal out there.

Mirror was growing fast even before the pandemic (no specific number was shared by management), and the pandemic of course led to a Cambrian explosion of interest in at-home fitness. In just two years since the launch, Mirror was expected to generate >$100 mn sales in 2020 at the time of acquisition. To give you a sense of the demand, three months after the deal call with the analysts, Lulu increased the expectation to >$150 mn sales in 2020. In terms of earnings impact, Mirror acquisition will be modestly dilutive in 2020 and management expects the acquisition to be accretive in 2021.

How does Mirror fit into Lulu story? Mirror’s customer gender mix is 50-50, so this can become a fertile ground for acquiring new customers for Lulu, especially men. Obviously, all Mirror instructors will wear Lulu products, and many of these instructors are presumably going to be Lulu ambassadors which can intertwine the symbiotic relationship among the ambassadors, the customer, and the company even further. Mirror gains access to not only Lulu ambassadors but also to a much better scale of customer awareness as well as a better marketing breadth under a brand umbrella that has a cult following. This should significantly reduce their CAC.

What can possibly go wrong? Well, the entire thing. What is the probability that we will remain infatuated with at-home online fitness classes when we are on the other side of the pandemic? Does the comfort and convenience of at-home studio outweigh a possibly more friendly environment with actual human connections in physical gyms? It is difficult to assign a specific probability to these questions, but I think it’s fair to say it is not a negligible probability that many of us will opt out of at-home fitness classes once the pandemic is over.

Even if it’s a powerful secular trend, there are questions about new competition. Peloton is a ~$40 Bn market cap company, and it is highly likely they may want to be much more than a connected-bike company. Peloton already allows non-cycling classes online which unlike Mirror, you can subscribe for $12.99/month without buying the hardware (the bike). If Peloton thinks “Mirror” is a resilient and powerful trend, they may come up with a similar hardware to bolster their product slates. Mirror’s scale simply pales in comparison with Peloton’s as it stands now (Mirror’s ~$150 mn revenue vs Peloton’s ~$3.5 Bn revenue in fiscal 2020).

Mirror is, by any measure, a VC-like investment. As it’s true for any VC investment, it can be zero in few years. Given the potential, I can be tempted to value the business at 2-3x times the value Lulu actually paid to acquire Mirror i.e. $500 mn. Even then, it’s 2%-3% current market cap of Lulu, so it doesn’t move the needle in terms of Lulu’s value as of today. I would most certainly not write a $10 Bn check today, but that doesn’t mean it cannot be a major success for Lulu someday. It can be, but I don’t think it’s prudent to assume success by default. We have very little idea about unit level economics of Mirror as Lulu hardly shared any data with analysts while acquiring Mirror.

Management, and its incentives

While Chip Wilson still owns ~8% outstanding shares of Lulu, he left the board in 2013 and currently has no direct involvement with the company or the board. In many ways, Mr. Wilson was a force of nature behind Lulu’s meteoric rise. But he also made headlines for some eccentric controversies. Following Wilson’s departure, Lulu was frankly not a very well-run company between 2014 and 2018, and the brand still remained relevant because of the power of the business model itself (the brand, distribution, and marketing).

Calvin McDonald joined Lulu in mid-2018, and so far, he has done an excellent job. He has provided the company challenging long-term goals, and Lulu seems well-positioned to hit and perhaps even exceed its goals of doubling DTC and men’s business as well as quadrupling international business. Given his former role at Sephora (CEO of Americas), he also seems the perfect person to lead Lulu if they want to expand their product breadth to areas such as Self-care, which he already outlined as one of the long-term goals.

In terms of incentives, annual executive bonus payout is determined by two operating performances: revenue (50%), and operating income (50%). Long-term performance based RSU is dependent on operating income (70%) and revenue (30%).

Lulu currently has no CFO. Patrick Guido, the former CFO, left Lulu in May 2020 and joined Asbury Automotive. Guido joined Lulu in April 2018, so it was a fairly short stint for him at Lulu.

Glenn Murphy, the former CEO of The Gap, chairs the board.

Final words

Let me repeat the first sentence. Lululemon Athletica is a fantastic company. The company is well run, and the brand is one of the most resilient ones in global retail. Apart from the optionality discussed earlier, Lulu’s balance sheet is incredibly resilient with close to net cash balance sheet which allows it to not only weather through tough times but also capitalize on acquisition opportunities such as Mirror.

But the current valuation is just too rich to my taste. There is a decent possibility that the fundamental implied projections in the model is too optimistic, and on top of that we need 25x terminal FCF multiple to generate ~7% IRR.

Even beyond the usual caveat of low interest rates in the long term to support such multiple, this lofty multiple demands long growth runway and durable competitive advantage. However, as Lulu becomes bigger and bigger and expands beyond yoga to other markets and product expansion, it may eventually face the big boys i.e. Nike/Adidas on their turfs more and more 10 years from now. Moreover, there is always a possibility of a Chip Wilson/Sara Blakely (see recommended readings) out there who may revolutionize the fashion of tomorrow’s world. Therefore, the possibility of erosion of competitive advantage is not a negligible or distant possibility for Lulu.

Granted, the optionality of Lulu is not well captured in the model, but I am reluctant to pay too much for that optionality without much data points or clarity at the moment.

Some can be tempted to argue whether valuation even matters these days. Of course, it does. I use a neat little trick to convince people that valuation does indeed matter. Just pick a company and add a zero after its share price integer, and then ask yourself whether the company would still be a great investment. Would Amazon be a great investment if it starts trading $32,000/share next week? Google at $17,000, anyone?

Given that there is a lot to like about Lulu, I will remain a close observer and will work on building convictions going forward.

If you are not a subscriber, click here to make sure you do not miss the next deep dive. The next deep dive will only be available for subscribers.

Earnings Updates

Recommended Readings/ helpful resource

1. The Story of Lululemon: Little Black Stretchy Pants (I don’t agree with everything he says, but it’s an interesting read nonetheless. This book again hits home how founder led companies think differently than management led ones, and how painful the transitions can be from founder to management)

2. Gavin Baker on Why category leading brick and mortar retailers are likely the biggest long term Covid beneficiaries

3. Napkin Math on Lululemon’s Mirror acquisition and Mazwood Cap on Lululemon (bullish)

4. Sahil Bloom on Spanx Founder Sara Blakely

5. Why Same Stores Sales is important by 10-k Diver

6. $350 jeans are dead. $100 leggings killed them. (WaPo)

7. r/lululemon(Good source to see informal comments on Lulu from real customers)

Disclaimer: All posts on “MBI Deep Dives” are for informational purposes only. This is not a recommendation to buy or sell securities discussed. Please do your own work before investing your money